When it comes to your financial role, no metric is more important than your credit score. Not only does this number affect your ability to get approved for a top travel credit card, it also affects the interest rate you pay on your mortgage, your ability to get a car loan, and many other aspects of your life.

If you’ve made a New Year’s resolution to improve your credit score in 2026, here are some strategies for successfully achieving it.

Learn the basics of credit scoring

Before we get into these tips, let’s first give a quick overview of what makes up a credit score. First, it’s important to note that there are two main credit scoring models: VantageScore and FICO.

While there are some differences between the two, they both attempt to numerically measure the same thing: how likely you are to repay borrowed money on time.

A lower score indicates a higher risk of defaulting on your loan, which lowers the amount of money or credit a financial institution is willing to lend you (or lowers your chances of getting approved for a loan at all).

On the other hand, a higher score indicates that you are less likely to default and therefore be able to handle larger loan amounts with fewer fees.

Both scores fall into the same range (300 to 850) and use the same general criteria:

- Payment history: How many missed or late payments have you made on your credit history?

- Amount owed: Often called your credit utilization ratio; a measure of how much of your available credit is currently being used

- Credit history length: The average age of your accounts with each lender

- new credit: How many new credits have you acquired recently, including the number of hard inquiries

- credit portfolio: The different types of accounts you have (credit cards, car loans, mortgages, etc.)

By paying close attention to these five items—especially the first two—you can do a great job improving your credit score.

Reward your inbox with the TPG daily newsletter

Join over 700,000 readers and get breaking news, in-depth guides and exclusive offers from TPG experts

Related: Your next credit card approval is in the hands of these 3 agencies

Check your credit report for inaccuracies

One of the most important things you should do is check your credit report for inaccurate information.

According to a 2024 survey by Consumer Reports and WorkMoney, 44% of consumers who successfully checked their credit report found at least one error. In many cases, these problems are not malicious (such as identity theft) but stem from simple mistakes (including confusing accounts or similar names).

Fortunately, there is an official process to eliminate these errors. This article from the Federal Trade Commission provides complete details on these steps, including how to request a free credit report each week.

Once you discover an error, submit a dispute letter directly to the credit reporting company; you can use the FTC’s sample for inspiration. The bureau must investigate complaints, often involving organizations that provide disputed information.

If this doesn’t help, the next step is to contact the information provider directly and file a complaint; again, the FTC provides a sample dispute letter for this purpose. Be detailed but concise and include copies of any documents that support your dispute.

While this process can be time-consuming, cleaning your credit report to remove any inaccuracies is an important step you can take to immediately improve your score, or at least prevent future errors that could cause your score to drop.

Related: How to check your credit score for free

Extend your available credit

Another way to improve your credit score in the new year is to expand the amount of credit you have available. This may seem counterintuitive: of course, more credit means more money to spend, and therefore more risk, right?

While that may seem true on the surface, remember that your credit utilization accounts for almost one-third of your FICO score (and a key part of your VantageScore). That’s why getting extra credit can improve your credit score.

There are two different ways to achieve this:

- Request a credit limit increase on an existing account: Some card issuers make it easy to request a top-up online, which usually won’t result in a hard query on your credit report.

- Apply for a new credit card: While this can cause difficult inquiries and temporarily lower your score, it can still provide you with new lines of credit (not to mention unlocking a potentially valuable welcome bonus). In the short term, this may outweigh the temporary decline and will almost certainly help in the long term.

Here’s an example of how it works. Let’s say you have a credit card with a limit of $5,000. Even if you pay it off in full each month, the average balance on the card will still be about $2,500 because you’re using it as your primary credit card and will continue to be charged for purchases as the payment due date approaches.

A general rule of thumb is to keep utilization below 30%, so in this case your utilization is well above that (50%).

Now, suppose you request an increase of $5,000 and are approved. Or, maybe you apply for a new card and get a $5,000 credit. With this action, your available credit has just increased to $10,000. As long as your balance stays within the $2,500 range, your utilization ratio will drop to 25%, which will cause your score to increase significantly over time.

However, this only works if you don’t use your new line of credit to spend more than you can afford. As long as your spending stays consistent, you can spread that amount across larger lines of credit, lowering your utilization ratio and improving your score. Credit cards don’t have to be a surefire way to get into debt. Make sure your purchases match your income.

Related: What is the difference between a hard pull and a soft pull on a credit report?

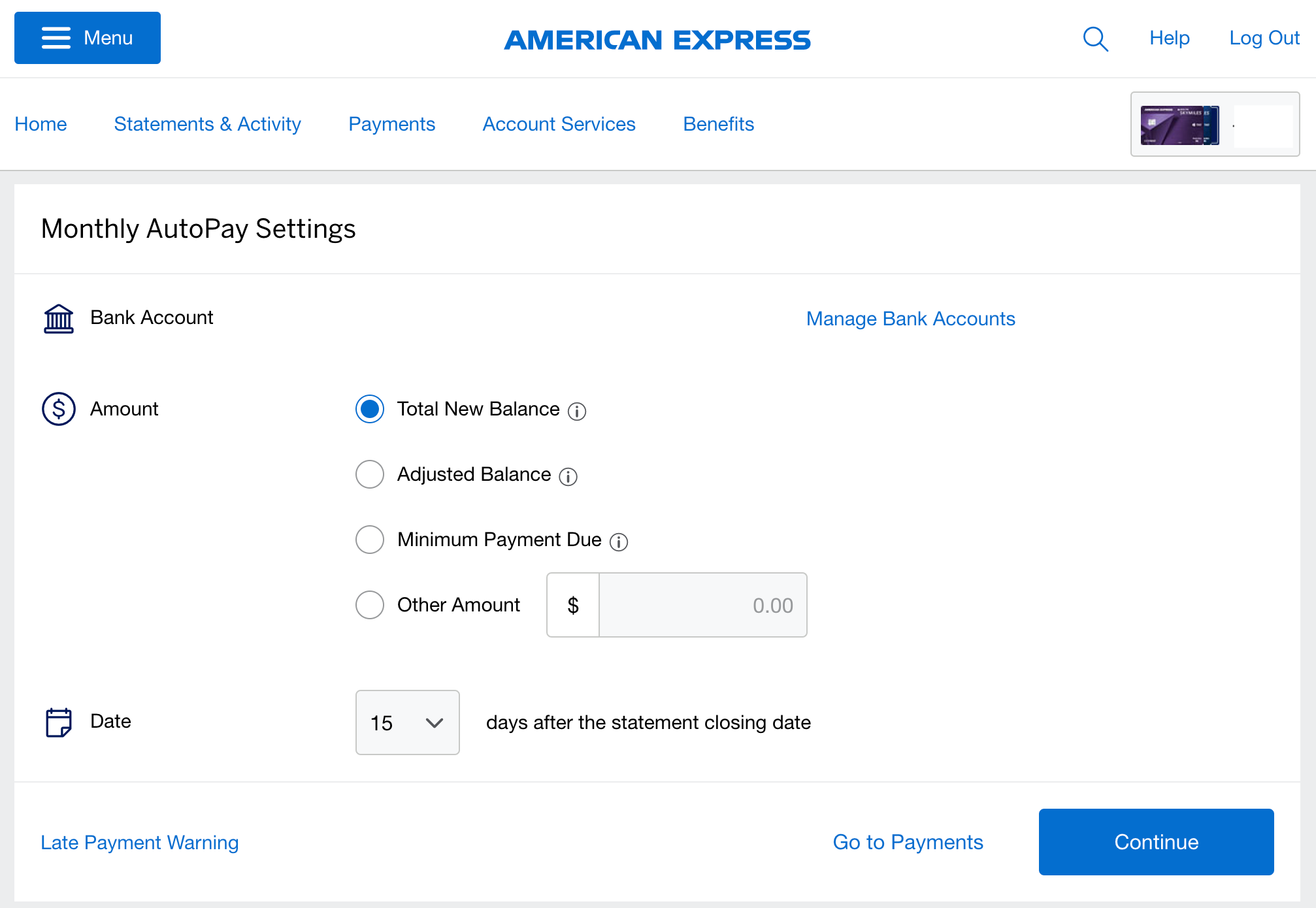

Set up automatic payments

If you’re prone to missing a deadline here or there, you should at least have a reminder on your calendar for when your credit card payments are due, and preferably enable automatic payments on your account.

As mentioned above, your payment history is the most important factor in determining your credit score, and even one late payment can significantly lower your credit score because it’s a sign that you may be struggling to pay off your balance.

By setting reminders or enabling automatic payments from your bank account, you can ensure that every payment will be processed on or before the statement due date.

The caveat to this, of course, is that you must keep enough funds in your bank account to cover the autopay balance. Otherwise, overdraft fees can eat into your income and still lead to late payments.

Budget to pay outstanding balances

TPG’s first commandment when it comes to travel rewards credit cards is: You should pay your balance in full.

If you carry a credit card balance each month, the interest charges you accrue can easily offset the value of the points or miles you earn on that card, if not more.

However, you may have an old debt from your freewheeling days in college, or you may choose to use an introductory 0% APR credit card or the deferred interest offer on a store credit card to fund a large purchase.

Don’t let these balances go unpaid. If you haven’t done so already, sit down and create a budget on how you’re going to pay off those balances to avoid (or minimize) your interest risk.

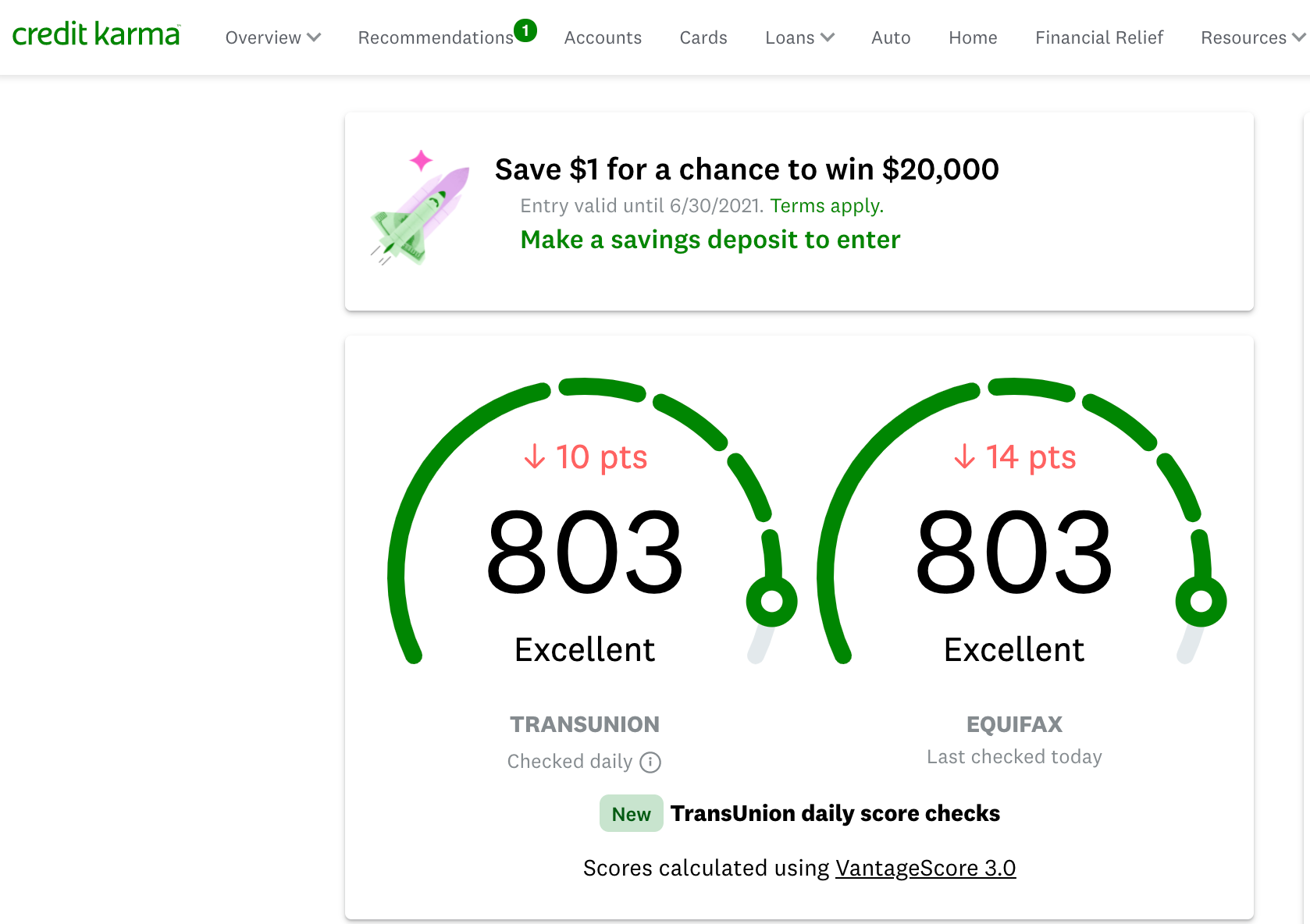

Sign up for credit monitoring

This last tip won’t necessarily improve your credit score immediately. Still, best practice is to keep a close eye on your score and quickly identify any issues that may arise. Sign up for a service that monitors your credit status and notifies you of any changes.

We like using Credit Karma, a free service that tracks your TransUnion and Equifax scores and allows you to view your credit report at any time. You can also set alerts for various things, such as report changes.

bottom line

Whether you’re new to the world of points and miles or have been doing it for a while, keeping your credit score high is one of the most important things you can do. This will increase your odds of approval for a top travel rewards credit card, expand your chances of getting an installment loan, and even lower the interest rates and fees you pay your lender.

If you’ve made up your mind to improve your score in 2026, we hope this guide has given you some concrete steps to improve your credit profile in the coming weeks and months.

Related: How to set up automatic payments for all your credit cards